Governor Tony Evers’ budget would overhaul the economic development tool known as tax increment financing, limiting TIF payments to developers and requiring more financial review of TIF plans. Unrelated school finance and property tax provisions also would lower TIF revenues. These proposals were pulled by the budget committee, but their significance and possible re-emergence as freestanding bills merit a closer look.

In proposing changes to Wisconsin’s tax increment financing law, Governor Tony Evers raised the question of how to manage risk within the main economic development vehicle for local governments in the state. The budget as proposed by the governor would put new requirements on municipalities seeking to use TIF to help pay for local projects and limit how TIF money could be spent to encourage development in a community.

As part of our ongoing research into this topic, we looked at the bill’s potential effects on how TIF is currently used to finance infrastructure and economic development. Though the Joint Committee on Finance has removed the TIF provisions from the budget, these proposals may be revisited in future legislation and also serve as an opportunity to examine broader TIF trends and policies.

TIF traditionally has been used to pay for public infrastructure such as streets or sewers (see box on page 2 as well as the recent Wisconsin Taxpayer, “Tax Incremental Financing on the Rise”), but Wisconsin municipalities may also use it to provide cash grants to developers as incentives to build in their community. These cash grants have drawn criticism in some communities from those who argue they can be an unnecessary public subsidy to private developers, but they are also defended as an investment to spur economic development that may not otherwise occur.

A review of available data suggests that developer grants have increased significantly over the years. Statewide in 2017, developer grants were 11% of total TIF spending, according to state Department of Revenue (DOR) data. However, a 2009 report by the Wisconsin Taxpayers Alliance (WISTAX), a predecessor to the Wisconsin Policy Forum, looked at 81 recently closed tax increment districts (TIDs) and found that 2.7% of expenditures were grants to developers. While the WISTAX report looked at spending by a smaller universe of TIDs over a longer period, that finding suggests an increase has occurred.

The budget bill would limit these grants, which local leaders typically use to encourage private development that otherwise might not occur in their community or to reimburse developers for borrowing associated with such development. For example, municipalities traditionally have financed TIF projects by borrowing money for infrastructure or other improvements that are needed to accommodate the desired development. The additional taxes generated by that development are used in turn to pay off the public debt. Over time, however, it has become relatively common for developers to borrow money to pay for the costs of TIF projects, taking on risk that had previously been assumed by the local government. Municipalities then pass on some or all of the increased tax revenues within TIF districts to the developer to help pay off the debt, with the payments classified in Wisconsin as “cash grants.”

How TIF Works |

| When a new tax increment district (TID) is created, the value of taxable property within it (its base value) is determined. Each taxing authority with jurisdiction in the district (the municipality, county, school district, sewerage district, and technical college) continues to collect taxes from that frozen base value throughout the life of the TID. However, as the property value of the TID increases from public and private investments, the increased tax revenue derived from the private development, or tax increment, is used to repay project costs and borrowing. |

The Evers proposal removed by the budget committee would limit cash grants to developers to 20% of a TID’s total project costs; as written, this would restrict both direct cash grants as well as reimbursements for developer-financed TIF. In 2017, 172 TIDs in the state, or 65% of TIDs that used cash grants, reported cash grants of 20% or more of spending. Existing TIF contracts presumably would not be affected by the proposed legislation, but these numbers provide a sense of the impact that such a proposal could have moving forward.

This is not the only impact the budget proposals put forward by Evers and rejected so far by lawmakers would have on TIF in Wisconsin. The legislation also would require alternative financial projections, or stress tests, be conducted prior to the approval of TIF plans. In addition, proposed changes to state property tax credits and school aids would indirectly lower the revenues of existing TIDs. In the pages that follow, we explore the potential impacts of each of these proposals and what they may mean for TIF in Wisconsin.

Limiting cash grants to developers

What are Cash Grants?

According to DOR, a cash grant is any cash payment the developer receives from the municipality or tax increment but does not have to repay. These payments are intended to fill gaps in financing, with supporters saying they are necessary to encourage developers to move forward with specific projects.

The payments also may be used as part of a developer-financed TIF agreement. In this type of agreement, a developer takes on debt that could be used for a variety of improvements such as land grading or a retention pond. Though the debt is not carried by the municipality, the borrowed amount is still repaid through the tax increment derived from rising property values in the TID.

Governor’s Proposal

As noted above, the governor proposed limiting cash grants to developers to 20% of a TID’s total project costs and lawmakers have removed the provisions. The 11% of TIF spending in Wisconsin that went to developers in 2017 made these outlays the third largest expenditure category for TIDs, after principal on long-term debt (40.9%) and capital expenditures (26.1%). (See Figure 1)

The use of cash grants to developers is relatively common and appears to have grown. In 2017, 264 of the 1,214 districts in the state, or 22%, reported making such payments, DOR data show. The developer grants for these specific districts averaged 45% of spending. As previously mentioned, developer grants in 2017 accounted for more than 20% of expenditures in 172 districts around the state. The 2009 WISTAX report found 11 of the 81 recently closed TIDs (14%) provided developer grants. Among this group, the average developer grant came to almost 20% of total expenditures.

These numbers do not provide a full picture of trends in developer grants since no comprehensive statewide data are available prior to 2016. Still, the figures do give a sense of how widespread developer payments are among districts in Wisconsin and how many future projects could be affected by the limits proposed by the governor and rejected so far by lawmakers.

In arguing for limits to cash grants, the Evers administration says the change would help ensure TIF boosts development through public infrastructure rather than subsidies for private investments. In particular, critics of TIF say some districts are created—and developer grants offered—in cases where the private development would have happened without any public contribution. They contend municipalities may feel pressure to provide TIF incentives to compete with neighboring communities by offering developer payments or other incentives that may not be needed to site the project in the area. Last, they say, the offer of TIF funds may incentivize development plans that the market would not otherwise support and arguably should not be pursued.

Opponents of the proposal say that municipalities should have the flexibility to judge for themselves whether and to what extent developer payments and other financing is needed to attract economic development. If used properly, they say, this tool can help municipalities proceed with projects that otherwise might fail to move forward, particularly in the case of sites and communities with blight, environmental concerns, or other factors that make development more costly and unattractive. Further, developer-financed TIF is seen by many municipalities as a tool for managing risk. Without it, local governments might have to take on more debt or forego projects.

Practices in Other States

The Evers proposal raises the question of how other states handle cash grants and incentives to developers and property owners. A look at neighboring states suggests Wisconsin may provide a greater degree of flexibility in how such grants can be used. The Lincoln Land Institute, a nonprofit that studies property taxes and land use, lists the grants as an eligible TIF expense in Wisconsin (provided the developer signs an agreement with the municipality) but not in Minnesota, Michigan, Iowa, or Illinois.

PROS AND CONS OF DEVELOPER FINANCING |

| Developer-financed TIF can decrease risk for the municipality and its taxpayers because they are not responsible for repaying the borrowing if the tax increment does not meet projections and cannot cover debt payments. However, this approach also can increase the total cost of the debt because developers typically must pay higher interest rates on loans than municipalities. |

At the same time, the other states allow TIF spending on costs such as land purchases and site preparations, which would allow developers to be reimbursed for those expenses in similar ways to how cash grants are used in Wisconsin. If the developer obtains the land or other improvements for less than a fair market price, the effect is essentially the same as a cash payment in that amount; both make the overall deal more profitable and attractive than it otherwise would have been.

In addition, these neighboring states permit some incentives that Wisconsin does not. In certain cases, all four neighboring states allow for the abatement of property taxes or personal property taxes as an economic development incentive. Wisconsin does not allow for property tax abatement, which would serve as another way to increase profits for a business and incentivize investment.

Stress Test

The governor’s budget also would require municipalities to run a “stress test” before officially creating a new TID. The state already requires municipalities to conduct an “economic feasibility study” prior to TID creation. The proposal rejected by the Joint Finance Committee would require “alternative growth projections” that account for how difficult economic conditions, such as slower than expected development, would affect growth in TID property values and the district’s ability to repay debt.

This recommendation seeks to address the number of distressed TIF districts statewide. Prior to 2015, municipalities could declare any TID created before October 1, 2008 as either “distressed” or “severely distressed” if its project costs were greater than the projected tax increment. A distressed TID could receive a 10-year extension on its maximum legal life (normally 20 to 27 years) and a severely distressed TID could have its life extended to up to 40 years total. State law no longer allows municipalities to designate TIF districts as distressed, but at the end of 2018 there were still 81 distressed and 18 severely distressed TIDs.

A TIF project gone awry can have a substantial impact on a community. In the Monroe County village of Warrens, for example, a TID created in 1998 to support the development of Three Bears Resort was designated as severely distressed after the resort closed and property values in the district plummeted by roughly 50% during the Great Recession. As a result, the village was forced to extend the TID past its maximum legal life of 27 years to pay off the debt. Alternative growth projections may not have made a difference—in this case village officials say they conducted stress tests. Still, requiring them for future projects might save at least some other municipalities from suffering similar fates.

Uses of TIF |

| Wisconsin municipalities may use TIF for several purposes: – Public infrastructure such as streets and sewers – Environmental remediation – Demolition – Professional services such as architectural drawings – Financing – Developer incentives, provided the municipality and the developer both sign a development agreement |

Academics have been recommending “risk assessments” prior to TIF implementation since at least 2012, having taken the idea from fiscal best practices in other areas. Among neighboring states, Minnesota has an analogous approach in which the county auditor is required to review the assumptions and financial analysis of TIF plans including the projected tax revenues, according to that state’s Department of Revenue.

We have found many municipalities already do alternative economic projections, whether on their own or through a consultant. For that reason, the proposal may not represent a large added burden for municipalities.

K-12 Aid changes would impact TIF

One aspect of the governor’s budget that has received almost no public attention is the impact of proposed changes to property tax credits and school aids on TIF district tax levies starting with the tax bills sent in December 2020 and paid in 2021. The Legislative Fiscal Bureau (LFB) projects TIF levies would fall by nearly $28 million, or 5.5%, for that year as a result of the changes proposed by Evers and rejected by the Joint Finance Committee, as shown in Figure 2.

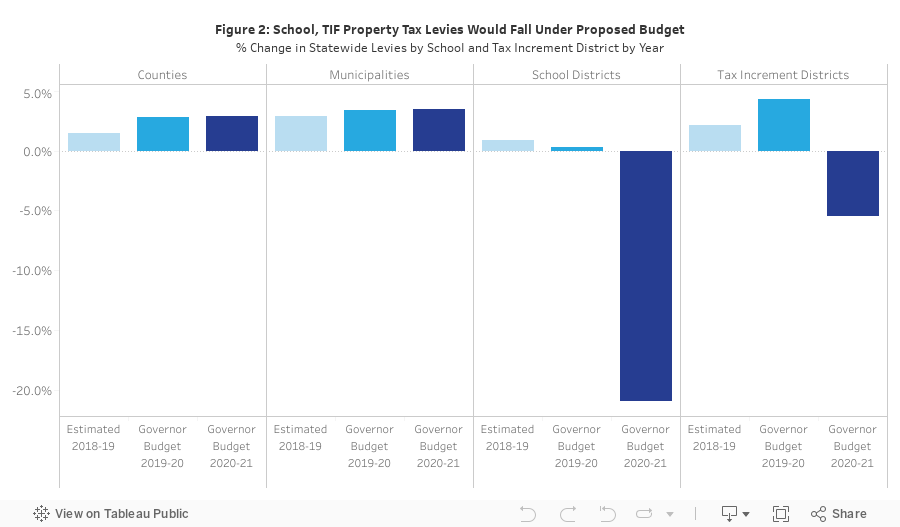

Explaining these potential impacts takes several steps. First, it is important to remember that TIF district tax revenues, or their increment, are determined in part by the combination of tax rates for the local municipality, county, school district, and any other jurisdictions authorized to levy property taxes. If there is a decrease or increase to a school district or other local rate, it also affects the TID and the revenues it generates to pay for infrastructure, debt service, and other costs.

In the second year of the budget, the Evers proposal would eliminate nearly $1.1 billion in two state property tax credits. Instead, the money from the credits would go toward increasing state aid to schools.

At the statewide level, the loss of the credits would not greatly affect property tax bills because the money would have to be used to reduce school property taxes. Under state law, school districts have caps on their total revenue from both state aid and local property taxes. For that reason, the rise in state K-12 aid to replace the property tax credit would require districts to decrease their property tax levies by an equivalent amount. That, in turn, would end up reducing the tax levies of school districts in the state by an estimated 20.9% on 2020-21 property tax bills, according to the LFB.

Though these changes would not affect statewide property tax bills, they would produce winners and losers. Home and business owners in some communities would end up paying more in property taxes and others less because of differences in how the tax credits are distributed compared to how school aid is awarded.

In addition, the lower school taxes would affect TIDs, which keep the tax increment in their boundaries that would otherwise be going to the local school district. Decreasing the school tax rate would lower the overall amount of levy generated by the incremental property value growth in the TID. In some communities, TIF levies would decrease more or less than the projected average drop of 5.5% statewide.

This is not the first time that state officials have proposed lowering property taxes in a way that would indirectly affect TID levies. A 2014 cut to technical college property taxes also affected TID collections and, in some cases, extended the time needed for districts to meet their obligations.

Conclusion

The governor’s proposed changes would have major impacts on the main local economic development tool in the state, lowering the revenues of existing TIF districts and potentially putting limits on the creation and structure of new TIDs. GOP legislative leaders have removed the TIF provisions from the budget bill but have not eliminated the need to debate the larger issues they raise.

There is still value in considering whether changes to TIF in Wisconsin are merited given its strong growth over the past decade and, if so, which ones. Previous WPF research found $472 million in TIF levies in 2017 alone, which was up 25% from 2007 after adjusting for inflation. As noted earlier, the practice of using developer grants appears to have increased even more quickly. As the example of communities like Warrens shows, the growing use of TIF makes it more critical to ensure that projects are successful and accountable to taxpayers.

At its heart, the present debate over TIF centers on evaluating the purpose of, and need for, these incentives. Is the private benefit for developers in conflict with the public interest or is it a necessary investment for achieving a public good? One tool for answering this question is data. In one positive change, the state Department of Revenue is making more TIF-related data available online, including district revenues, expenditures, and fund balances. However, providing more data is only beneficial if the data are used to make better public decisions.

The additional TIF requirements proposed by the governor could come with both benefits and costs. The proposal to require stress tests for new TIF projects might help to flag potential risks at a relatively modest price to municipalities and developers. On the other hand, the stress tests could mean another hurdle and at least some additional cost in the TIF approval process, particularly for municipalities without the expertise to perform such tests on their own.

The proposal to limit cash grants would mean a loss of flexibility for local leaders seeking to promote economic development and manage risk. For some projects, it might help to contain the ultimate cost to the public and prevent public grants to private developers who do not need such assistance. In other cases, however, it might mean that a municipality carries more risk or that no project is carried out at all. Ultimately, lawmakers and the public have to decide whether they would be willing to forgo some deals to reduce the potential for unnecessary developer payments and, if so, the appropriate level of tradeoff. Either way, no single proposal can eliminate the need for municipal officials to vet and negotiate TIF agreements aggressively.

| The lead author of this report, Rachel Ramthun, is the Wisconsin Policy Forum’s 2018-2019 Todd A. Berry Fellow. The fellowship supports research that is directly relevant to key policy issues confronting state and local governments in Wisconsin and was named after Todd Berry, who led the Madison-based Wisconsin Taxpayers Alliance (a predecessor to the Wisconsin Policy Forum) for more than 20 years. |

Finally, the governor’s proposal to overhaul school funding in Wisconsin would have substantial effects not just for education but for the state’s overall system of property taxes and credits. That plan goes well beyond the scope of this report, but it is worth noting its potential impact on TID collections and finances. The plan serves as a reminder that big changes to the state’s tax system often affect local governments and must be considered with care.