As Wisconsin faces severe economic turmoil in the weeks and months ahead, the state is in a better position to confront the challenges than it was before the Great Recession. From handling long-term debt to immediate bills, the state established a sounder financial footing in 2019 than at any point in years. Despite the gains, however, Wisconsin remains no better than the average state on many measures and like other states will need federal aid to help cope with reduced tax collections and massive increases in emergency spending.

Facing what could be a prolonged period of deep economic disruption, the state of Wisconsin’s finances are much stronger now than at the onset of the last recession in 2007. Though the fiscal hardship still will be severe, today the state at least can draw on supports that were absent or depleted then, including a relatively strong unemployment insurance fund and other cash balances that can help to pay the state’s short-term bills. The reserves will be needed given the new reality of diminished state tax collections and the need for increased spending on jobless benefits, social services, and a wide variety of crisis-related emergency needs.

Not all aspects of the state’s financial condition are strong. State debt levels and debt payments have improved substantially in recent years but remain higher than at the beginning of the Great Recession, particularly for highway and transportation borrowing. Per capita state debt is also higher in Wisconsin than in the average state.

Though the state has made solid progress on key indicators of fiscal health, Wisconsin still falls in the middle of the pack among all states on measures such as the amount it has in budget reserves as a share of expenditures. A notable exception is its unusually well-funded and designed pension system, which is better situated than most states at least to begin absorbing recent huge losses in financial markets.

Wisconsin Policy Forum reports have detailed the sizable increases in the state’s cash balances in its general and rainy day funds. While policymakers have debated options for using those balances, the Forum has repeatedly stressed the value of maintaining them as a cushion against unexpected economic shocks. As this report shows, however, a recession as deep as the one that is likely emerging could still exhaust these reserves.

In addition, it is important to note that the general fund covers only about half of the state’s overall operating budget. State leaders must also consider long-term assets and liabilities such as debt and retiree benefits. To provide a more complete picture, this report details a number of indicators of the state’s fiscal health to give policymakers and the public a better sense of the state’s strengths and weaknesses as it navigates the monumental challenges ahead.

SHORT-TERM HEALTh improves

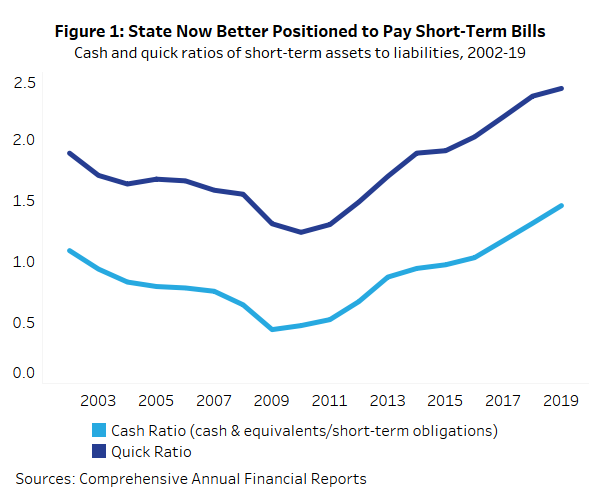

A paramount concern for the state in a time of crisis is paying its bills and covering its immediate financial needs. With respect to these near-term concerns, the state of Wisconsin as of last summer was clearly in its best shape since the wake of the 2001 recession.

This report examines these issues using the state’s Comprehensive Annual Financial Report (CAFR), which covers all of the state’s revenues and expenditures, not just those contained within the general fund. The CAFR details the state’s assets and liabilities and uses national accounting standards that factor in delayed payments and other accounting maneuvers that can exaggerate the state’s financial health in its more commonly cited budget documents.

To cover bills coming due within weeks, the state can draw on cash and assets equivalent to cash (money market accounts and certificates of deposit) as well as certain other liquid investments such as U.S. Treasury bills, a form of short-term debt. Here we compare these liquid assets held by the state as of June 30 of last year (the end of its 2019 fiscal year) with the obligations that were due within the next 60 days.

This “cash ratio” in June stood at the highest level in our records going back to 2002 – 1.46 – meaning the state had almost one-and-a-half times more cash and other liquid assets than it had short-term bills and obligations (see Figure 1). In 2009, during the worst of the Great Recession, this ratio fell to .44, suggesting the state had less than half of the liquid assets needed to pay its short-term obligations easily.

Figure 1 also shows progress had been made in the state’s “quick ratio,” which adds receivables such as federal aids to the assets in the cash ratio. With these short-term assets as of June at nearly two-and-a-half times short-term obligations, the quick ratio was also at its highest level since at least 2002.

A third ratio, known as the “current ratio,” adds less liquid assets such as fuel and other inventories. The state’s current ratio (not shown) has taken an almost identical trajectory to the quick ratio over the years. Though these gains are positive, the state could still experience cash flow issues given the severity of the current crisis and the fact that balances in one part of state government cannot necessarily be used to support spending in another.

Unemployment Fund on the rise

More than any one single factor, the condition of the state’s jobless fund was responsible for the deterioration in the state’s cash position between 2002 and 2009 and its subsequent recovery in recent years (see Figure 2). With unemployment claims rising at historic levels today, the strength of the fund is an essential question.

In June 2002, the fund charged with paying benefits to unemployed workers had a net position of $1.59 billion (including $1.46 billion in cash and equivalents). Even as the economy improved in the following years, the fund’s net position shrank to $783.9 million by June 2007 (with even less in cash), leaving it unprepared for the deep recession that followed. By the summer of 2009, the fund had run out of cash and in the following years the state was forced both to borrow more than $1 billion from the federal government to make payments to workers as well as raise unemployment taxes for a time to pay off the loan.

In the decade since, the unemployment rate has fallen and the state has paid back the federal loan and built up just over $2 billion (including $1.87 billion in cash) in the jobless fund as of June 2019. This shift has placed one of the state’s key programs for responding to a recession in a much better position to address the current crisis. For more on the unemployment fund see our April 2019 research brief.

Despite this progress, however, a recent U.S. Department of Labor report found that, as of Jan. 1, Wisconsin’s jobless fund ranked 30th in the country on a key measure of readiness for weathering a recession. The indicator looks at whether the state’s reserves meet a federal recommendation of being able to cover one year of benefit payments at a rate equal to the average of the three highest claims years within the past two decades. The state fell just barely short of that recommended level and as a result Wisconsin would not normally qualify for interest-free federal loans for the program.

The state undoubtedly will see changes soon to unemployment benefits from both federal legislation and state action aimed at helping jobless workers – for example, Gov. Tony Evers has already waived the requirement that unemployed workers conduct at least four weekly search actions. An initial federal response also provides $1 billion in aid for state unemployment programs nationally.This amount is relatively little given that some large states such as California and New York have little in reserves but the act does provide interest-free loans for state funds through December 31.

General Fund grows

As the state’s economy and tax collections grew in recent years, cash balances also increased in the state’s general fund and rainy day fund (see box at the bottom of the page) and in the University of Wisconsin System, marking an improvement from the 2002 to 2009 period. In those years, the state shifted money from the state transportation fund to balance its general fund budget, which supports priorities such as aid to school districts and health care for low-income residents.

Despite the progress, however, Wisconsin remains behind most other states in terms of having cash and liquid assets on hand to cover its bills. A 2018 study from the Mercatus Center at George Mason University used 2016 data to compare the state’s cash, quick, and current ratios to those of other states and found that Wisconsin ranked 39th for short-term financial health. This “cash solvency” rank was down slightly from 38th the previous year, suggesting other states were making as much or more progress than Wisconsin.

BUDGET HEALTH bolstered

The state budget has also seen improvements since the last recession in its ability to cover its annual expenses with its annual tax collections and to overcome unexpected setbacks, such as lower-than-projected revenue growth or higher-than-expected spending.

Drawing on the state’s CAFR, we compared total annual revenues to expenditures from all state funds (not just the general fund), a metric known as the “operating ratio.” For 2019, the state’s ratio was 1.05, meaning that the state had enough revenues from taxes, federal aid, and other sources to cover its spending that year (see Figure 3). The 2019 figure was among the state’s highest since 2002 though it was somewhat higher in 2012 through 2014.

This indicator suggests the state has strengthened its budget by moving away from its past practices of using one-time pots of money, accounting gimmicks, and other maneuvers to spend more than it takes in. The Mercatus Center also found that Wisconsin’s operating ratio was above the national average for states in 2016.

A big part of this post-recession improvement came from the state’s unemployment fund, which saw demand for benefits decrease and revenues rise because of payroll tax increases. In balancing the general fund budget, state leaders also relied less than they did from 2002 to 2010 on money from segregated funds and one-time sources such as infusions from the transportation fund, a fund for compensating injured patients, and a settlement with tobacco companies.

Another measure of state budget health looks at its yearly surplus or deficit, or the state’s annual change in net assets. This indicator tracks the change in the value of all state assets such as cash, investments, receivables, and buildings after subtracting for any outstanding debt used to acquire those assets. The state’s total net assets hit a low for the period in 2010 and have been rising since then (see Figure 4).

The state scored relatively well on the Mercatus rankings for budget strength, which are calculated by combining states’ scores for operating ratios and surplus or deficit. The state ranked 18th nationally according to 2016 data.

DEBt levels moderate

Even before adjusting for inflation, overall state debt at the end of last year stood at the lowest level in a decade, partially offsetting substantial increases in debt that occurred during the last recession and in the decade leading up to it (see Figure 5). That holds down debt payments and also provides the state with greater capacity to borrow to address capital needs for infrastructure such as buildings, highways, and bridges.

As of December 2019, the state had $12.63 billion in bonds and other debt outstanding, down 2.5% from 2018 and marking the fourth consecutive year of decreases. Without even adjusting for inflation, debt is now down $1.57 billion, or 11.1%, from its peak of $14.2 billion at the end of 2012, according to figures from the state’s annual disclosures filed with federal securities regulators.

A significant share of the decrease since 2012 ($379.5 million) was in general obligation debt. This debt is backed by the full faith and credit of the state of Wisconsin, which means that the state has pledged to use all its resources, including its tax revenues, to repay them. The state also reduced by $604.3 million its debt for municipal water quality projects and by about $333 million the bonds issued to fund liabilities within the state pension fund and for unused sick leave that employees can draw on to pay for health care in retirement.

Going forward, however, the state could see renewed upward pressure on borrowing and not only from the crisis. After four years of below average levels of investment in state facilities, the 2019-21 budget authorized more than $1.9 billion for capital projects, the largest amount since 2001 even after adjusting for inflation (for more see our August 2019 report).

In a time of economic stress, however, the state is most immediately affected not by its total debt outstanding but by its annual debt payments, which reduce the funds available for other spending priorities and put could lead to tax increases. The state has long sought to keep annual debt payments made with General Purpose Revenue, or GPR (mainly income and sales taxes), to less than 4% of total spending.

During the last recession, the state kept GPR debt payments artificially low by delaying some principal payments. But that had the effect of increasing subsequent payments even more. Figure 6 shows by fiscal year 2014, GPR debt payments had risen to 4.9% of total spending. (These figures are calculated using reports aligned with the state budget, not the CAFR.)

After several years above the 4% target, GPR debt payments have fallen back below it to 3.4% in 2019, according to figures from the Legislative Fiscal Bureau and Department of Administration. The drop in debt service reflects the fact that the great majority of the decrease in overall state debt since 2012 has been in borrowing that is paid off using GPR funds. Though the state’s overall levels of outstanding debt and debt payments have moderated in recent years, borrowing for highways and other transportation projects remains a major concern. The debt paid off using transportation fund revenues such as vehicle registration fees has fallen somewhat since its peak of $2.11 billion at the end of 2015 but at $1.77 billion this form of outstanding debt remains almost as high as it was in 2012.

Debt payments are also consuming a larger share of the revenues within the transportation fund, leaving less money available to pay for other ongoing state and local transportation needs. As Figure 7 shows, debt payments rose from 7.1% of transportation fund revenues in 2000 to 19.3% in 2019.

The 2019-21 state budget includes $390 million in new revenues for the transportation fund over the two years, mostly through higher vehicle registration fees. Those additional revenues should help to both cover debt payments as well as help limit future borrowing. However, as with many other aspects of state finances, the current crisis will impact the fund’s revenues by substantially lowering gasoline purchases and fuel tax collections.

Despite the progress made in recent years, as of 2016 the Mercatus Center still reported higher per capita debt levels in Wisconsin than those of the average state nationally.

LONG-TERM HEALTH MORE BROADLY

The state’s fiscal condition has also improved in terms of long-term liabilities that go beyond just debt to include benefits owed to active employees and retirees. In general, Wisconsin performs relatively well in this area because of its fully funded state pension fund and its relatively manageable retiree health care obligations (see our March 2020 report on the Wisconsin Retirement System). Here several metrics taken from the CAFR can offer context.

The state had a modest increase in its long-term liabilities per capita to $2,871 on June 30, 2019, up from $2,838 the prior year. After adjusting for inflation, these liabilities were down somewhat from their peak in 2012 and in the Mercatus rankings were substantially lower than the national average.

The state also saw a drop in the ratio of its overall liabilities to assets (a decline is positive in this case), reversing the rise that happened in the 2000s. State liabilities on June 30 of last year amounted to 33.9% of state assets, the lowest share in Forum data going back to 2002 (see Figure 8).

One final metric to examine is the ratio of the state’s net assets to its total assets, with a higher ratio indicating greater health. After falling as low as -18% in 2010, this ratio had climbed back to 5.2% as of the end of June, the highest level in our data going back to 2002.

The Mercatus Center report found that as of 2016, Wisconsin ranked 24th for long-term financial health, a measure that included the three metrics above (long-term liabilities per capita, liabilities to assets, and net asset ratio). That was an improvement over the state’s 2015 rank of 27th. Wisconsin ranked much better – sixth nationally – for unfunded pension and retiree health and life insurance liabilities as a share of the annual income of state residents.

CONCLUSION

Our analysis of key financial metrics shows state finances have improved almost across the board since the last recession. The state showed greater strength last year than at any point since at least 2002 on important indicators ranging from its short-term cash reserves to its ratios of liabilities to assets.

Yet, despite this progress, Wisconsin remains no better than average on most measures when compared to other states. In fact, the Mercatus Center ranks the state 26th in its overall fiscal ranking, which combines the measures discussed above. Though the ranking draws on somewhat dated 2016 figures, the criteria and data used do not change greatly from year to year. Only in the area of pension and retiree liabilities does Wisconsin truly stand out in a positive way from other states.

As state leaders determine how to respond to an economic downturn of still-to-be-determined length and potentially historic severity, they will benefit from the state’s improved fiscal condition. Nevertheless, as tax collections slow and the state faces huge increases in demand for unemployment benefits and social services – as well as pressing requests from local governments struggling to address their own fiscal crises – the cushion built during previous years is likely to evaporate very quickly. Wisconsin will have many potential demands on its general and rainy day fund reserves, including financing health care or other coronavirus-related responses, as other states have started to do.

An important question is the response of the federal government and its prioritization of direct financial assistance for affected businesses as well as state and local governments. There is no doubt that the fiscal impacts of the current crisis will be more than most states and localities can bear without federal aid. The extent to which that assistance is broadly and meaningfully forthcoming will significantly impact Wisconsin’s ability to navigate these uncharted fiscal waters.

Perhaps the only good news is that as difficult as the current financial picture appears, it could actually be worse. When the last recession arrived, Wisconsin was in many ways among the least prepared states in the nation. Today, at least, the state is average on most measures and in the case of funding its retirement benefits, is actually a national leader.

These gains were eked out over years of tough budgets and better-than-expected tax collections, and ironically they were preserved in recent weeks by legislative gridlock that prevented passage of proposals that would have eroded a portion of the state’s reserves. This confluence of difficult decisions and good fortune may blunt at least some of the heavy financial blows for the state in the months to come.

|

Surplus Saved By Gridlock With tax collections at the time exceeding projections, just weeks ago Democratic Gov. Tony Evers and leaders in the Republican-held Legislature were debating what to do with a historic surplus in the state’s general and rainy day funds. |