For the sixth straight year, property values in the state grew, underlining the benefits of the expanding economy. But new construction numbers have yet to see the same recovery, raising renewed questions about using them as the sole factor to limit local property tax increases.

New state figures show property values in Wisconsin rose last year by the fastest rate since before the Great Recession—a welcome reminder of the economic recovery. However, while some parts of the state have seen strong growth over the past decade, property values in parts of northern and central Wisconsin have yet to recover fully.

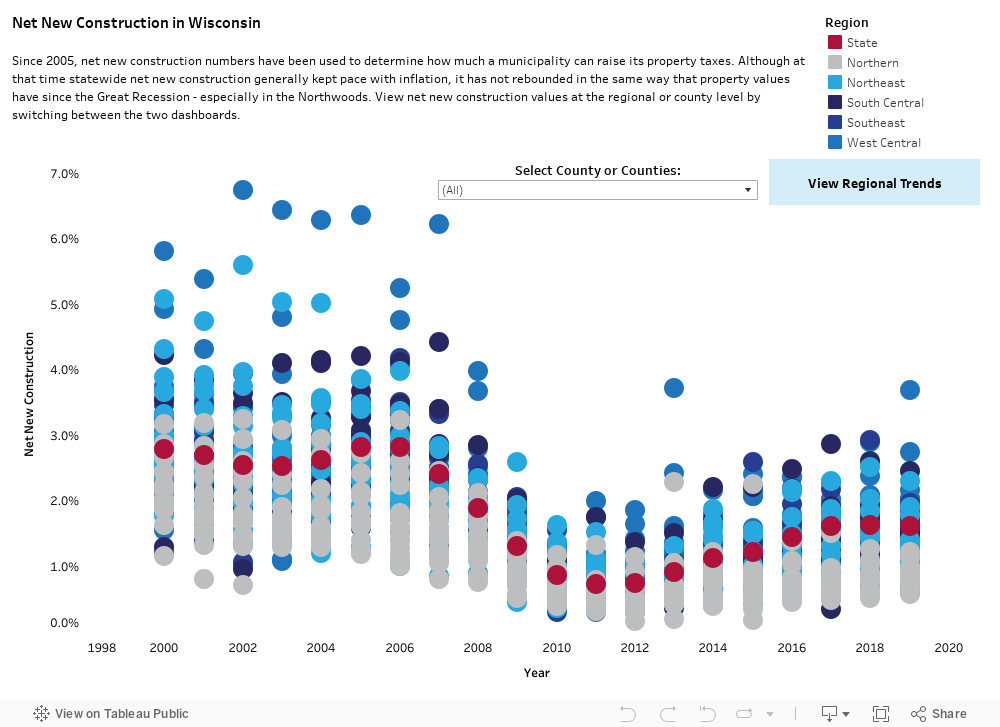

Also, the good news about the overall increase in property values is tempered by the fact that most of that growth comes from appreciation of existing properties. New construction in the state is growing slowly and is not contributing to rising property values the way it did before the Great Recession. The growth in property values from new construction—or lack of it—matters for both taxpayers and elected officials, as the state uses it to limit property tax increases for local governments across Wisconsin.

Each year, the Department of Revenue publishes data at the municipal, county, and state level on two important metrics: net new construction and equalized property values. We take a broad look at these numbers here, in advance of a more detailed upcoming report on state property taxes and values. From 2018 to 2019, equalized property values increased for the sixth straight year, rising 5.7% to $580.9 billion statewide, and producing a new high in nominal dollars for the third straight year. Meanwhile, the percentage increase in values attributed to net new construction amounted to 1.6%.

The state “equalizes” property values across all of its municipalities each year to account for differences in how local officials assess properties and how recently they have done so. This is important to ensuring that different communities pay their fair share of property taxes within overlying units of government like schools or counties.

Since 2005, annual property tax increases for Wisconsin municipalities, counties, and technical colleges to cover ongoing operations generally have been limited to the rate of net new construction. That means the limit varies widely by community. For example, in the most recent data, Madison’s net new construction rate was 2.23%, while Racine’s was just 0.14%.

New Construction and Levy Limits

Given that Wisconsin relies heavily on the property tax to fund local government, it matters that the state also has relatively tight limits on its growth. The link between levy limits and net new construction was first established in 2005, when the rate of net new construction statewide was 2.82%; the rate has not reached 2005 levels since, and has been below 1.75% in every year since 2008.

In addition, state officials initially included a “floor” for the property tax limits that allowed local governments to increase their levies each year by the greater of their rate of new construction or a specified percentage, which was never lower than 2%. The floor was removed in 2011, however, tying increases—with some exceptions—to new construction alone.

In 2018, the statewide rate of net new construction (1.60%) barely surpassed the relatively low rate of inflation from January 2018 to January 2019 (1.55% as measured by the Consumer Price Index). Less than a quarter of all municipalities had rates of net new construction above the rate of inflation, including only seven of the 20 most populous cities and villages (Madison, Kenosha, Eau Claire, Janesville, Wauwatosa, Wausau, and Menomonee Falls).

Since 2014, the south central portion of Wisconsin—which includes Madison, Janesville, and Beloit—has had the highest rate of net new construction of any part of the state; 2019 was the third straight year that the region enjoyed a rate above 2%. The west central region of the state (Eau Claire, La Crosse, and Wausau) had a rate of 1.85% in 2019, its highest since 2008 and the only other regional rate to beat inflation. The northern region (Superior, Minocqua, and the Northwoods) had a rate of just 0.85% and remained under 1% net new construction for the 11th straight year.

Despite some regional success in both south and west central Wisconsin, none of the five regions saw more than a third of their municipalities experience a new construction rate above inflation. While some individual municipalities have higher rates of net new construction, all five regions have yet to return to the growth rates seen in the late 2000s.

A similar story can be told at the county level. Clark, St. Croix, and Dane counties had the highest rates of net new construction, and represented three of just 22 counties that outpaced inflation. Meanwhile, none of the 20 counties located north of Wausau had net new construction rates above 1.5%.

Residential Values and Recovery

While net new construction numbers continue to lag since the Great Recession, overall equalized property values have grown more steadily. From 2018 to 2019, equalized values grew by more than $31 billion, or 5.72%, the highest growth rate since the 5.81% growth in 2007. According to the Department of Revenue, all 72 Wisconsin counties experienced a growth in equalized values for the first time since before the Great Recession.

Of the $31.4 billion total increase in equalized values, $22.6 billion resulted from market value increases, while $8.8 billion was due to new construction. Residential property grew by $24 billion, or 6.1%, which is the highest rate of growth since a $31 billion increase (10.0%) in 2006. Commercial property increased $5.7 billion (5.2%). Residential parcels account for 71% of all property values statewide and commercial parcels for 19.9%. Combined, residential and commercial property values account for about two percentage points more of statewide property values since 2000, but their share of the total has remained relatively stable since the Great Recession.

For the second straight year, Dane County ($69.9 billion) led the state in equalized values (for more on this trend, read Focus 2018 #15). Equalized values in 34 of Wisconsin’s 72 counties grew by at least 5% between 2018 and 2019, but every county in the state saw at least a 1% increase. (See Figure 2.) St. Croix and Sheboygan counties each surpassed $10 billion in equalized values for the first time.

Despite statewide growth for six straight years, not every county has seen equalized values recover to pre-recession levels. For example, while Dane County (the state’s fastest-growing county) surpassed its 2009 equalized value peak in nominal dollars in 2015, Milwaukee County’s total of $67.2 billion in equalized property values remains $1 billion below its 2008 peak.

Thirteen counties had equalized values in 2019 that were still below their values from 2008, even without accounting for inflation. Besides Milwaukee County, this total includes two central Wisconsin counties (Adams and Green Lake) and 10 Northwoods counties (Vilas, Oneida, Price, Sawyer, Ashland, Iron, Burnett, Washburn, Forest, and Bayfield).

Takeaways

Statewide equalized values have increased for six straight years, and the majority of the state’s population now lives in a municipality or county where land is valued higher than ever before, at least in nominal dollars. That said, even in a strong period of economic growth, the increase in property values from net new construction remains below pre-recession levels.

The slow and uneven growth in new construction raises the question of whether the state should reconsider its use as the sole factor in limiting the growth in property taxes. Tying tax increases to net new construction has slowed the growth of municipal and county levies to the benefit of property owners. However, linking increases year after year to a factor that lags inflation for many Wisconsin communities makes it difficult for them to maintain service levels over time.

An additional concern—discussed in our 2018 report A Growing Divide—is the potential creation of a permanent set of “winners and losers” among the state’s municipalities. That could occur if high-growth communities—by virtue of that development—can increase tax levies and invest in priorities like transportation and parks that encourage more growth, while low-growth communities with fewer resources to invest are locked into a cycle of lagging development.

Property tax limits and their link to net new construction are not necessarily the most important factors contributing to or limiting growth at the local level. Still, recent trends suggest state lawmakers and the governor may want to at least consider whether these factors are creating unintended consequences that need to be addressed.