Last year, the state of Wisconsin’s “hidden deficit” fell by more than one-third – the largest decrease in decades in percentage terms. The state’s main fund ended 2019 in the best shape on record, a more than $2 billion improvement over 2011. Yet on this measure, Wisconsin continues to trail nearly every other state.

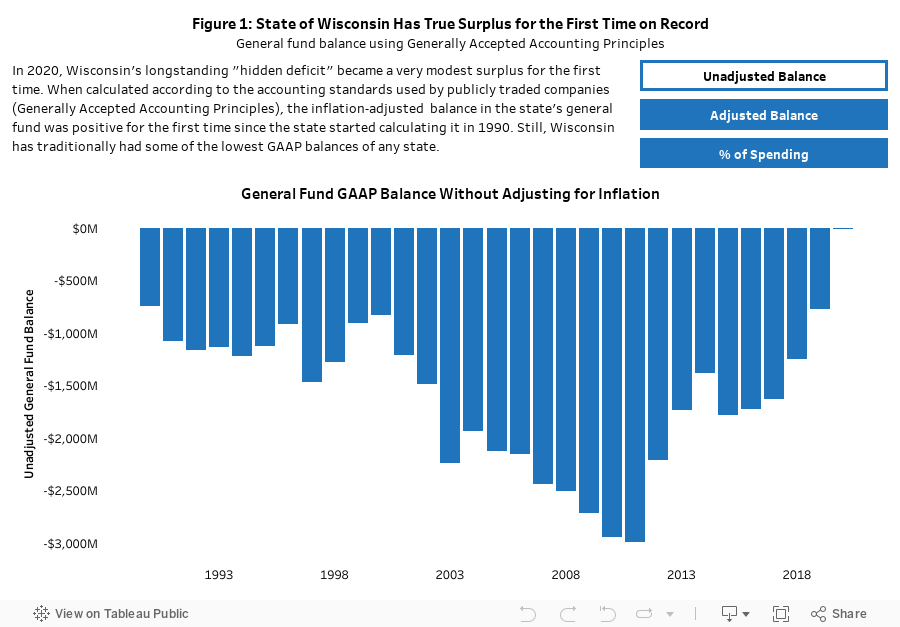

With tax growth strong, the negative balance in Wisconsin’s main fund shrank to a new low in fiscal year 2019, raising the possibility that the state might eliminate the decades-old financial hole that could be thought of as its “hidden deficit.” Newly released financial statements report that on June 30 of last year the state’s general fund had a negative balance of $773.5 million – the lowest level after adjusting for inflation in records going back to 1990.

The $480.1 million improvement in 2019 – a 38.3% decrease over the previous year’s ending balance of $1.25 billion – means the state has less need today than ever before to push its current bills into the next budget, putting Wisconsin in a better position to weather future financial storms (see Figure 1). In addition, the state’s 2019 financial statements show improvements in many other areas.

At the same time, Wisconsin remains one of only three states with a negative general fund balance at all. In addition, decisions made as part of the 2019-21 state budget mean the state could slide backward if the strong growth in tax collections falters.

The Hidden Deficit

The figures in this brief come from the Comprehensive Annual Financial Report (CAFR) the state published last month. Like the financial statements of publicly traded companies, this report uses Generally Accepted Accounting Principles (GAAP) that differ from the accounting methods used in state budget documents.

Under GAAP or accrual accounting, expenses are recorded when the state commits to them even if the payment is not made until later (for more see this brief from last year.) State budget documents use cash accounting and only book expenses when the state actually pays the money. Under cash accounting, the state general fund and its closely linked rainy day fund had a combined $1.74 billion left over at the close of the fiscal year on June 30, 2019.

The CAFR tells a different story, one in which the general fund’s liabilities outweighed its assets. In 2019, the general fund had revenues of $27.87 billion from sources such as income and sales taxes. To support priorities such as education and health care, the fund had expenditures and net transfers out of a combined $27.39 billion. That yielded an annual surplus of $480.1 million that improved the general fund balance.

However, because the general fund started 2019 with a negative balance of $1.25 billion, it ended the year still $773.5 million in the red, or 3% of expenditures. On the bright side, as recently as 2011 the general fund deficit was $2.99 billion ($3.40 billion after adjusting for inflation), or 13.5% of spending. If the general fund balance improves as much in the next two years as it did in 2018 and 2019, it would close 2021 with a positive GAAP balance for the first time.

Despite this progress, it is important to note that state Controller’s Office data show only two other states ended 2018 with a negative general fund balance – Illinois and Kentucky. Also, Wisconsin’s $133 per capita deficit for 2019 compares to a surplus in three neighboring states (see Figure 2). Illinois does have a much larger per capita deficit than Wisconsin’s but that state’s budget troubles are some of the nation’s worst.

The negative balance matters because it represents spending the state has committed to and will have to pay for in the following year. If Wisconsin’s economy and tax collections keep growing, the state can handle these unpaid bills. In a downturn, however, the negative balance adds to the state’s short-term expenses.

Explaining the deficit

The general fund has had a negative GAAP balance going back to 1990, when Wisconsin started calculating it. In one sense, there is no one budget item or group of them that is responsible for the negative balance because it is the sum of all the past decisions that caused money to flow into and out of the general fund. In the same way, the balance in a family’s savings account reflects all of its past deposits and withdrawals.

However, several decisions by the state stand out. First is the timing of state aid and property tax credits that are paid to local governments. For years, the state has been committing to pay certain amounts in a given year but not actually paying much of the totals until July, the month after the state’s fiscal year ends.

This accounting maneuver has allowed state officials of both parties to take credit for more spending in a given year without affecting the balance shown in the general fund using cash accounting. For example, the general fund’s June 2019 balance is lowered by $491.2 million after adjusting the state’s cash accounting system to reflect delayed payments for state aid to local governments known as shared revenue. Accounting for delayed payments for state property tax credits lowers the balance by an additional $809.6 million.

Much of the progress in reducing the state’s GAAP deficit has come from increasing its cash balances in the general and rainy day funds. The combined cash balance in those funds has risen more than $1.6 billion since the end of 2011, when it was just $102.2 million.

In addition, the state has brought the general fund GAAP balance closer to the cash balance by limiting excess state income tax withholding that is later refunded to taxpayers. The GAAP balance takes into account the next year’s refunds, but they artificially boost the cash balance. In 2014, the governor and Legislature adjusted income tax withholding tables to reduce excess withholding.

There’s no guarantee the state will continue to make progress in reducing its hidden deficit. In fact, the current 2019-21 budget is projected to reduce the general fund’s cash balance substantially, which could in turn lower the GAAP balance. So far this year, state tax revenues have shown strong growth, which if sustained might help maintain the general fund balance. However, at some point growth in the economy and tax collections will falter. That could bring a return to growth in the deficit similar to 2001, when the recession that year caused the negative balance to grow after several years of improvements.